News

New Stratus Energy Announces Significant Acquisition in Venezuela and Corporate Update

January 2, 2024

NEW STRATUS ENERGY ANNOUNCES SIGNIFICANT ACQUISITION IN VENEZUELA AND CORPORATE UPDATE

NOT FOR DISSEMINATION IN THE UNITED STATES OR FOR DISTRIBUTION BY ANY UNITED STATES NEWS DISTRIBUTION SERVICE

Calgary, Alberta, January 2, 2024 – New Stratus Energy Inc. (TSX.V - NSE) (“New Stratus”, “NSE” or the “Corporation”) is pleased to announce the closing of the acquisition (the “Acquisition”) of a 50% indirect interest in GoldPillar International Fund SPC Ltd. (“GoldPillar”), a private entity organized and existing under laws of the British Virgin Islands, which has acquired a 40% equity participation (the “Equity Subscription”) in a joint venture company, Petrolera Vencupet, S.A. (“Vencupet”), which holds the oil production rights for the fields named “Adas”, “Lido”, “Limon”, “Leona”, “Oficina Norte” and “Oficina Central”, all located onshore in the Anzoategui and Monagas States in Eastern Venezuela (the “Fields”). Petroleos de Venezuela S.A. (“PDVSA”), the Venezuelan national oil company, through its subsidiary Corporacion Venezolana de Petroleo S.A. (“CVP”), owns the remaining 60% of the share capital of Vencupet. As consideration for the Acquisition, New Stratus will be making a significant capital investment to complete a reactivation program for up to 246 wells in the Fields, by way of a six-month €60 million (US$65.8 million) revolving line of credit to Vencupet through GoldPillar, as described in further detail below. Factoring repayments from the sale of oil and products under the financing agreement, New Stratus expects that its indirect maximum capital exposure under the facility at any point in time will be approximately US$25 million.

As consideration for securing and presenting this opportunity to New Stratus, a finder’s fee (“Finder’s Fee”) is payable to Mr. Franco Favilla (“Favilla”), an Italian national and formerly the beneficial owner of 100% of the share capital of GoldPillar, in the amount of US$8.5 million, with US$4 million paid at closing and US$4.5 million payable in installments over 24 months from closing.

Acquisition Highlights

- Fields: 794.2 km2 onshore Venezuela

- Term: initial term ending in December of 2035; will apply for an extension until 2050

- Credit Facility: GoldPillar will provide a six-month €60 million revolving line of credit to Vencupet for a total period of four and a half years; indirect maximum capital exposure of NSE under the facility at any point in time will be approximately US$25 million

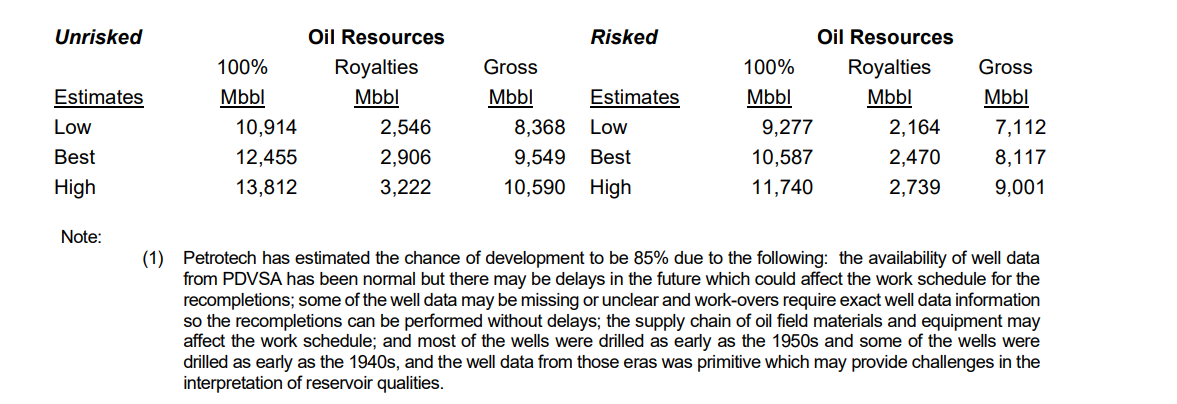

- Contingent Resources – Development Pending(1):

- Best Estimate 100% Unrisked of 12,455 thousand barrels (Mbbl) and 100% Risked of 10,587 Mbbl

- Best Estimate forecast production of approximately 7,400 barrels per day

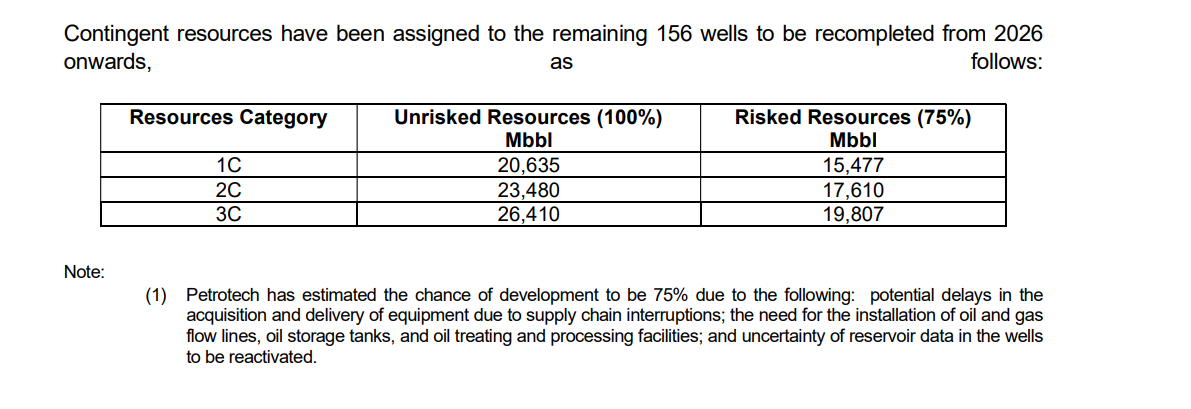

- Contingent Resources – Development Unclarified(1):

- Best Estimate 100% Unrisked of 48,905 Mbbl and 100% Risked of 30,323 Mbbl

- Four Revenue Streams for GoldPillar:

- Oil Production Revenue from a 40% working interest in the Fields

- Services Fees as general contractor to restart production in the Fields

- Financing Fees from providing the upfront capital to finance the capital expenditure requirements for the Fields

- Oil Trading Fees from commercializing the production from the Fields

Fields

The Fields are located onshore in the Eastern Venezuela Basin and have an aggregate area of 794.2 km2 . Due to a lack of investment and working capital, the Fields are not currently producing. The Fields were most recently on production in 2015, when production averaged approximately 800 to 1,000 barrels of oil equivalent per day (boepd). In 1960 when the Fields initially came on production, the Fields achieved peak production of approximately 60,000 boepd. Production from the fields has consisted of light and medium crude oil, heavy crude oil, conventional natural gas, and natural gas liquids.

Vencupet’s assignment of the oil production rights to the Fields has an initial duration of 25 years, ending in December of 2035. Under current arrangements with PDVSA, Vencupet will be applying for an extension of such rights for 15 additional years, that is until the year 2050. A subsidiary of GoldPillar will be the exclusive contractor (the “Contractor”) for operation activities on the Fields and will undertake a reactivation program to restart production.

The reactivation program consists of reactivating 246 wells, with 90 wells being reactivated in 2024 and 2025 and the remaining 156 wells being reactivated in 2026 and beyond. The Contractor will perform conventional workovers in each well with the goal of returning the wells to primary production. By reviewing the available technical and geological data, the Corporation expects there will be opportunities to recover shut-in and by-passed oil in the previously active Fields. The Corporation expects commercial production to begin in Q1 2024. The reactivation program is based on a pre-development study involving field visits and reservoir analysis.

Contingent Resources

Based on the reactivation program described above, the Fields include the contingent resources outlined below. There is uncertainty that it will be commercially viable to produce any portion of the resources.

Contingent Resources (subclass: development pending) for the first 90 wells to be reactivated in 2024 and 2025

The contingent resources have been assigned to one zone per well for each of the 90 wells. These 90 wells were mostly drilled in the 1950s and 1960s, and there is well completion data for 46 of the 90 wells to be recompleted. The estimated total capital costs for the 90 well reactivation program is US$89.2 million in the low, best and high cases, which will be funded from cash on hand and production revenue. The forecasted gross production for the 90 wells in the best estimate case is approximately 7,400 barrels of oil per day based on the historical production decline curves for each well. The following table sets forth the net volumes for these contingent resources:

Contingent Resources (subclass: development unclarified) for the remaining 156 wells to be reactivated from 2026 onwards

Contingent Resources (subclass: development unclarified) for additional zones in 46 of the first 90 wells to be reactivated in 2024 and 2025

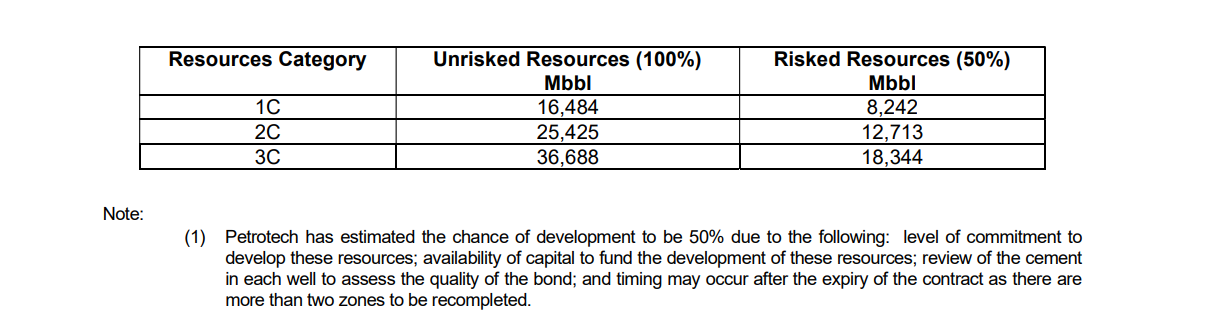

As described above, contingent resources have been assigned to one zone per well in the first 90 wells. As there are more zones to be recompleted, these contingent resources have been assigned based on the continuation of the reactivation program in other available zones in 46 of these wells after the first zone is depleted, as follows:

Resources Category Unrisked Resources (100%) Mbbl Risked Resources (50%) Mbbl 1C 16,484 8,242 2C 25,425 12,713 3C 36,688 18,344 Note: (1) Petrotech has estimated the chance of development to be 50% due to the following: level of commitment to develop these resources; availability of capital to fund the development of these resources; review of the cement in each well to assess the quality of the bond; and timing may occur after the expiry of the contract as there are more than two zones to be recompleted.

Total Contingent Resources (subclass: development unclarified)

The significant positive and negative factors relevant to the estimates above are as follows: (i) by reviewing the available technical and geological data, the Corporation expects there will be opportunities to recover shut-in and by-passed oil in the previously active Fields; and (ii) the geological and geophysical data (i.e. 2-D and 3-D seismic data) is limited because the Fields are old (with the first discovery dating back to the 1930s) and new seismic acquisition will be required to explore the remaining areas of the Fields.

The risks and level of uncertainty associated with the recovery of the contingent resources comprise the following:

- Although U.S. sanctions have lifted in October 2023 for a period of six months, there is no certainty that this moratorium will continue. If the United States imposes sanctions on Venezuela again, there is no certainty the production from the Fields can be marketed or commercialized.

- There is uncertainty in obtaining all the necessary geological and technical data for all the drilled and completed wells. Without the exact data, it will be challenging to perform work-overs to reactivate these wells.

- In order to complete the reactivation program, GoldPillar will require experienced engineers, geologists, production and operating staff. If GoldPillar is unable to retain such personnel, then the start-up of shut-in oil and gas fields and the maintenance of production may prove challenging.

Acquisition Overview

Pursuant to the Acquisition, the Corporation is acquiring its indirect interest in GoldPillar and the Fields as follows:

- NSE, through a wholly-owned subsidiary, has entered into a 50/50 corporate joint venture named “Desarrolladora de Oriente Oil & Gas Ltd.” (“DOOG”), a British Virgin Islands company, Favilla in exchange for the payment of the Finder’s Fee;

- DOOG holds 100% of the share capital of GoldPillar;

- GoldPillar, which has been qualified by PDVSA to be a shareholder of Venezuelan joint venture companies holding oil and gas exploration and production rights in the country, holds 40% of the equity of Vencupet; and

- Vencupet is owned 40% by GoldPillar and 60% by CVP, and holds the oil production rights for the Fields.

Acquisition Framework and Revenue Streams

The overall acquisition framework consists of four distinct revenue streams, as outlined below:

- As a 40% working interest owner in the Fields, GoldPillar will receive revenue associated with the production from the Fields.

- Pursuant to an operation services agreement, a subsidiary of GoldPillar will act as the exclusive general contractor for Vencupet to restart the production in the Fields and development of the required surface infrastructure. The services under the agreement will be provided at agreed upon rates plus an administration fee.

- Pursuant to a financing agreement, GoldPillar will provide a six-month €60 million (US$65.8 million) revolving line of credit to Vencupet for a total period of four and a half years. Borrowings under the facility will be repaid through the assignment by PDVSA of volumes of crude and products equivalent to 60% of the amount of the advances plus interest with instructions to use such proceeds for amortizing the debt. Borrowings under the facility will bear interest at a rate of 9.87% per annum. Factoring repayments from the sale of oil and products under the financing agreement, the Corporation expects that its indirect maximum capital exposure under the facility at any point in time will be approximately US$25 million.

- Pursuant to a crude oil and product commercialization agreement, an affiliated oil trading company will commercialize nominated crude and petroleum products by PDVSA, which proceeds will be for the account of DOOG and subsequently used to repay the borrowings under the revolving line of credit, to fund operating costs, to pay royalties and taxes, and to pay dividends to the shareholders of Vencupet. Oil trading fees resulting from such commercialization activities will be for the account of GoldPillar.

Any disputes under the agreements referred to above will be referred to international commercial arbitration in Caracas, Venezuela under the rules of the International Chamber of Commerce.

Advisors

Cormark Securities Inc. and Horizon Capital Partners LLC acted as financial advisors to the Corporation with respect to the Acquisition. Dentons Cardenas & Cardenas and Dentons Canada LLP acted as legal counsel to the Corporation with respect to the Acquisition.

Canaccord Genuity Corp., Echelon Wealth Partners Inc., Paradigm Capital Inc. and Hannam & Partners (UK) are acting as financial advisors to the Corporation.

Corporate Update

Mr. Wuilian Mauco has resigned from the board of directors of the Corporation. Accordingly, the Corporation has accepted his resignation and will commence a search to fill the vacancy on the board of directors. The Corporation wishes Mr. Mauco all the best in his future endeavours.

Contact Information:

Jose Francisco Arata

Chairman & Chief Executive Officer

ygrene.sutartswen@atarafj

Wade Felesky

President & Director

ygrene.sutartswen@ykselefw

Mario Miranda

Chief Financial Officer

ygrene.sutartswen@adnarimm – (416) 363-4900

Forward-Looking Information

Certain information set forth in this news release constitutes “forward-looking statements”, and “forward-looking information” under applicable securities legislation (collectively, “forward-looking statements”). All statements other than statements of historical fact are forward-looking statements. Forward-looking statements may be identified by the use of conditional or future tenses or by the use of words such as “will”, “expects”, “intends”, “may”, “should”, “estimates”, “anticipates”, “believes”, “projects”, “plans”, and similar expressions, including variations thereof and negative forms. Forward-looking statements in this press release are based on the Corporation’s current internal expectations, estimates, projections, assumptions and beliefs, which may prove to be incorrect. Forward-looking statements are not guarantees of future performance and undue reliance should not be placed on them.

In respect of the forward-looking statements contained herein, the Corporation has provided them in reliance on certain assumptions that it believes are reasonable at this time, some or all of which may prove to be incorrect. Accordingly, readers should not place undue reliance on the forward-looking statements contained herein. Such forward-looking statements necessarily involve known and unknown risks and uncertainties, which may cause actual performance and financial results in future periods to differ materially from any projections of future performance or results expressed or implied by such forward-looking statements. There can be no assurance that forward-looking statements will prove to be accurate, and actual results and future events could differ materially from those anticipated in such statements. New Stratus undertakes no obligation to update forward-looking statements if circumstances or management’s estimates or opinions should change except as required by applicable securities laws. Actual results, performance or achievement could differ materially from those expressed in, or implied by, these forward-looking statements and, accordingly, no assurance can be given that any of the events anticipated by the forward-looking statements will transpire or occur, or if any of them do so, what benefits may be derived therefrom.

Oil and Gas Advisory

This news release includes resources information attributable to the Fields effective as of November 30, 2023 prepared by Petrotech Engineering Ltd., which is an independent qualified reserves evaluator. The reserves information was prepared in accordance with the Canadian Oil and Gas Evaluation Handbook (“COGE Handbook”) and National Instrument 51-101, Standards of Disclosure for Oil and Gas Activities.

Contingent resources are those quantities of petroleum estimated, as of a given date, to be potentially recoverable from known accumulations using established technology or technology under development but are not currently considered to be commercially recoverable due to one or more contingencies. Contingencies are conditions that must be satisfied for a portion of contingent resources to be classified as reserves that are: (a) specific to the project being evaluated; and (b) expected to be resolved within a reasonable timeframe. Contingencies may include factors such as economic, legal, environmental, political, and regulatory matters, or a lack of markets. It is also appropriate to classify as contingent resources the estimated discovered recoverable quantities associated with a project in the early evaluation stage. Contingent resources are further categorized according to the level of certainty associated with the estimates and may be subclassified based on project maturity and/or characterized by their economic status.

There are three classifications of contingent resources: low estimate, best estimate and high estimate. Best estimate is a classification of estimated resources described in the COGE Handbook as being considered to be the best estimate of the quantity that will be actually recovered. It is equally likely that the actual remaining quantities recovered will be greater or less than the best estimate.If probabilistic methods are used, there should be at least a 50% probability that the quantities actually recovered will equal or exceed the best estimate.

Contingent resources are further classified based on project maturity. The project maturity subclasses include development pending, development on hold, development unclarified and development not viable. The contingent resources acquired in the Acquisition are classified as development pending and development unclarified. A maturity class of development pending describes the status of a project addressing all or part of a known accumulation where project activities are ongoing to justify or optimize future commercial viability. The critical contingencies have been identified and are expected to be resolved within a reasonable timeframe. A project may be assigned a maturity subclass of development unclarified if it is still under evaluation (e.g., a recent discovery) or requires significant further appraisal to clarify the development potential and where the contingencies may not have been fully defined.

References to "unrisked" contingent resources volumes means that the reported volumes of contingent resources have not been risked (or adjusted) based on the chance of commerciality of such resources. In accordance with the COGE Handbook for contingent resources, the chance of commerciality is solely based on the chance of development based on all contingencies required for the re-classification of the contingent resources as reserves being resolved. Therefore unrisked reported volumes of contingent resources do not reflect the risking (or adjustment) of such volumes based on the chance of development of such resources.

Statements relating to resources are deemed to be forward-looking statements, as they involve the implied assessment, based on certain estimates and assumptions, that the resources described exist in the quantities predicted or estimated. The resources estimates described herein are estimates only. The actual resources may be greater or less than those calculated. The estimated volumes of contingent resources contained herein do not represent fair market value of the contingent resources. There is no certainty that it will be commercially viable to produce any of the resources.

BOEs may be misleading, particularly if used in isolation. A BOE conversion ratio of 6 thousand cubic feet (Mcf) per 1 barrel (bbl) is based on an energy equivalency conversion method primarily applicable at the burner tip and does not represent a value equivalency at the wellhead. As the value ratio between natural gas and crude oil based on the current prices of natural gas and crude oil is significantly different from the energy equivalency of 6:1, utilizing a 6:1 conversion basis may be misleading as an indication of value.

Neither TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.